(Here is my take on this article Therapeutic Use of Cannabis and Cannabinoids A Review JAMA Network, 11/26/25. On a personal side, I use CBD to help me sleep, and with a little (5%) addition of THC, it is a great anxiety calmer – Sally Torgeson, AnCan Blood Cancer Moderator & Multiple Myeloma Coach)

Unapproved Cannabis

The FDA has NOT approved the cannabis plant (botanical marijuana) for any medical use or indication.

Because it is classified as a Schedule I controlled substance under federal law, the FDA has not found it to be safe or effective for the treatment of any disease or condition [1.1, 1.7].

It is currently illegal to market CBD by adding it to food or labeling it as a dietary supplement in interstate commerce [2.1, 2.5].

FDA-Approved Cannabinoid Drugs

The FDA has approved a small number of prescription drugs containing either a purified cannabis-derived compound or synthetic cannabinoids:

Epidiolex (Cannabidiol or CBD): The only FDA-approved drug that contains a purified substance derived directly from the cannabis plant. It is approved to treat seizures associated with Lennox-Gastaut syndrome, Dravet syndrome, and Tuberous Sclerosis Complex in patients one year of age and older [1.8, 2.1].

Marinol and Syndros (Dronabinol): Contain synthetic Δ9-tetrahydrocannabinol (THC). Approved for:

Nausea and vomiting associated with cancer chemotherapy in patients who have not responded to conventional antiemetic treatments [2.2, 2.3].

Anorexia associated with weight loss in patients with HIV/AIDS [2.3].

Cesamet (Nabilone): Contains a synthetic substance that is chemically similar to THC. Approved for chemotherapy-induced nausea and vomiting [1.1, 2.3].

Regulatory Context

The FDA maintains its authority to regulate products containing cannabis or cannabis-derived compounds, even those derived from hemp (cannabis with less than 0.3% THC), under the Federal Food, Drug, and Cosmetic (FD&C) Act [1.4].

The FDA supports the development of new drugs through proper clinical trials to ensure they meet standards for safety and effectiveness [1.1, 2.4].

FDA-Approved Cannabinoid Drugs and Their Conditions

* Nausea and vomiting caused by cancer chemotherapy (when other antiemetics have failed) * Anorexia (loss of appetite) associated with weight loss in patients with HIV/AIDS

Cesamet (Nabilone)

Synthetic cannabinoid (similar to THC)

* Nausea and vomiting caused by cancer chemotherapy (when other antiemetics have failed)

Key Takeaway

Epidiolex is the only drug approved that contains a substance derived directly from the Cannabis plant (CBD). It represents the strongest evidence for cannabinoid efficacy in reducing seizure frequency in certain rare forms of epilepsy [1.1, 1.2].

The synthetic THC compounds (Dronabinol and Nabilone) are used primarily as a last resort for severe nausea/vomiting related to chemotherapy and for appetite stimulation in AIDS patients [1.2, 2.8].

The FDA has not approved the use of the whole cannabis plant for any medical condition, stressing the importance of standardized, tested pharmaceuticals for patient safety and proven effectiveness [1.7].1

Off-Label Use vs. Unapproved Use

1. Off-Label Use (Legal and Regulated)

This applies only to drugs that the FDA has already approved.

What it is: Using an FDA-approved drug (like Epidiolex, Marinol, or Cesamet) for a condition, dose, or patient population that is not specifically listed on the drug’s official label.

Legality: It is legal for a licensed physician to prescribe an approved drug for an off-label use if they believe it is medically appropriate for their patient.

FDA Position: The FDA does not regulate the practice of medicine; however, the manufacturer cannot market or promote the drug for the off-label use. The safety and efficacy for the off-label use have not been verified by the FDA’s rigorous testing process.

Example: A doctor prescribing Marinol (Dronabinol), which is approved for nausea from chemotherapy, to a patient for chronic pain. The drug is approved, but the condition (chronic pain) is not on the label.

2. Unapproved Use (Non-FDA Approved Products)

This applies to the cannabis plant itself and most CBD/cannabinoid products on the market.

What it is: Using the whole cannabis plant (botanical marijuana) or non-FDA-approved cannabis-derived products (like most CBD oils, edibles, or topicals) for any medical purpose.

Legality:

Federal: The whole plant is a Schedule I controlled substance and is not federally approved for any medical use.

State: Use may be legal under state medical or recreational cannabis laws, but this does not change its status as an unapproved drug under federal FDA law.

FDA Position: The FDA considers these products unapproved drugs and/or illegally marketed products (especially when CBD is added to food or marketed as a dietary supplement), as they have not been tested for safety, effectiveness, or quality assurance.

Example: A patient using a CBD tincture (which is not Epidiolex) to treat anxiety, or using THC flower to help with multiple sclerosis symptoms.

To correspond with Sally, please send an email to info@ancan.org, and we’ll be sure to send along.

CNTV’s recent video features an interview with AnCan founder, Rick Davis. He explains that he started AnCan after his own diagnosis in 2007, after realizing inadequate support options, especially for those in remote areas. AnCan aims to eliminate barriers to entry for its various support groups, which range from cancer to chronic diseases. AnCan empowers patients to “Be your own best advocate” by providing them with the knowledge to speak confidently with their healthcare providers and offering peer-to-peer support.

“Someone I once loved gave me a box of darkness” –Mary Oliver

I was at a 12-Step-oriented workshop about grief recently, and it made me think about Men Speaking Freely (MSF). We are vaguely aware of grief in all MSF groups, it hangs over us, and we have at times focused on some specific griefs/losses, such as vitality, or a longer life. It is commonly thought that not thinking about a loss, not talking about it is the manly thing to do. Here in MSF we get relief by sharing our common losses with each other.

The presenter of that workshop, Marcia C., had some ways to specifically talk about grief that were new to me. She gave me permission to use some of her material here. She pointed out some types of losses that I hadn’t realized. For example, the loss of who I would have been if cancer didn’t happen, the grief of estrangement, loss of work, of status, of friendship; the loss of never having had something, that of aging, of trust, or of giving up something.

She said there is “unacknowledged grief” when such losses are never fully brought to consciousness. When I looked at her long list of examples I saw many that I have. We ought to watch for unacknowledged grief.

She described “non-finite” grief, which has no end-point other than death. Ours could be in that category, since as time goes by our loss increases instead of lessens.

Marcia said, ‘’Sharing your grief is a way to receive validation and compassionate witnessing. It can help you begin a path to healing and/or finding a way to live with grief.

Consider the questions below:

1. Are there griefs you haven’t realized you have or have been afraid to face?

2. Are there griefs about which you’d like to share?

3. Do you have grief practices that might be helpful to others?

4. Make a list of griefs you’ve experienced.

5. Choose a tool from the list that might help you process your grief.”

That list of “tools” was long; it included things like: write a letter or poem describing our loss…Create a ritual of letting go…Share with others who have had similar losses…Visit a place that is meaningful…Make or buy a talisman that helps you feel protected…Dance, run, yell to get your feelings out of your body…Plant something in remembrance or as a new beginning…Start a new tradition…Do an intentional funeral… These are ways to bring acknowledged, unacknowledged, and non-finite grief out for a conscious conversation. Moving from covert to overt, with the goal of making a relationship with the loss, and getting rid of the unconscious silent prolonged scream that I, for example, think I harbor.

We think of grief as emotional, but in “Dealing With the Physical Impact of Intense Grief” by Batya Swift Yasgur, the author describes the variety of physical reactions to grief. Ranging from elevated blood pressure to takotsubo cardiomyopathy — sometimes called “broken heart syndrome” — which is a “stress response that balloons the heart.” We often wonder about the reaction on our immune system, and its implications to our overall survival. In fact, probably nearly all our systems react to grief in some way.

There is a fairly new grief-related diagnosis in the Diagnostic and Statistical Manual and the International Classification of Diseases, describing a “persistent and pervasive grief response” that goes on longer than a year., and is now called Prolonged Grief Disorder. In order to be diagnosed with Prolonged Grief Disorder, a person must experience at least three of eight additional symptoms that include “disbelief, intense emotional pain, feeling of identity confusion, avoidance of reminders of the loss, feelings of numbness, intense loneliness, meaninglessness, or difficulty engaging in ongoing life” according to Columbia University’s Center for Prolonged Grief. For an adult to meet the criteria for a PGD diagnosis, the death of a loved one must have occurred at least one year ago, and the symptoms must be present most days since the loss and nearly every day for at least the last month.

Our situation is different from losing a loved one (although it includes that) and waiting for the grief to go away. Instead of a major loss which goes farther and farther into the past, our major loss is in the future. We have sort of a reverse Prolonged Grief Disorder. For instance, I expect my losses to get worse and worse until death.

AnCan Foundation, the innovator of virtual support groups, is coming to our 10th Anniversary in less than 10 months. We’ve grown – about one-third of US nonprofits fail in that time, and we have flourished. Starting with 3, or was it 4, meetings, AnCan now boasts 33 virtual monthly events for 16 different conditions. If that’s not evidence enough, annually we serve around 7,000 live; approx. 33,000 through our recordings, and we have close to a half-million who make contact with the AnCan logo somehow or other annually. That’s a lot. Watch out for our new Impact Report that’s in the works.

It’s certainly more than one person can handle. In fact, it’s more than myself, a volunteer, plus 4 contract people and an outside bookkeeper can handle. I’m not the only volunteer. I am so honored and privileged to say it’s more than around 100 volunteers can handle, and we could not manage without your efforts – much gratitude.

For some time, the executive function has been too much for me to manage alone, even with the help of our volunteer Executive Board made up right now of Bill Franklin, David Muslin and Stuart Jordan – btw, we’re looking to add to that too. We’ve been looking to hire executive help and the perfect solution has presented itself.

Some of you may be aware of the term, Fractional Executives – The Charity CFO just ran a podcast. AnCan has been fortunate enough to find one who knows us intimately. Courtesy of the USAF and subsequently, extensive consulting experience at The Mitre Corporation, our Board President, Bill Franklin, is voluntarily reducing his hours at Mitre to take on a contract position of 16-20 hours a week with lil’ ol’ AnCan.

As our Board President since August 2021, Bill knows all the ins and out, he’s seen us grow, and most significantly he’s willing to work with me! Bill’s also looking to phase out of Mitre and find new challenges as he approaches retirement. AnCan provided a great solution and we welcome him as our new Chief Operating Officer.

Bill will continue as Board President as well as assuming oversight over many of the operating and administrative duties, from finance and control to insurance, compliance and many special projects – viz. the Impact Report !?! To be honest, Bill’s been doing a lot of this informally but can now spend legitimate time a couple of days a week to help us put our ship, or maybe we should say ‘our bird’, in better order.

Personally, I am thrilled and excited. There’s no one I can think I would rather work with. I welcome him sharing this job with me, and keeping me on the straight and narrow as he has done since joining the Board many years ago. One other person to thank – another aviator, Bill’s wife Misa. If she hadn’t gotten on his case for spending many volunteer hours with AnCan, Bill wouldn’t have come up with this great solution.

Welcome aboard, Sarge… or should I say, Mr. Prez! AnCan welcomes Air Relief

A couple of weeks back, we posted Medicare Health Insurance Choices that explained the differences and pitfalls between traditional Medicare Part A and B plus Medigap insurance plans to Part C, Medicare Advantage. Click the link earlier in the previous sentence if you missed it.

As many already know, there is a Part D that covers drug costs. It is either purchased as a separate plan or rolled into Part C Advantage. Drug coverage is significantly changing this year, and AnCan has learnt that many of our participants are not yet aware. Hardly surprising because CMS as well as the various stakeholders like Payers and providers have done very little to let us patients know. Why should they? – we’re only the ultimate consumer!

The same cannot be said of JnJ who started educating patient advocate organizations this past May. In October and November JnJ created more education that includes a webinar and a round table coming up hosted by NAMAPA, the National Association for Medication Access and Patient Advocacy. Likely you have never heard of them. I hadn’t and it hardly rolls off the tongue. Nonetheless, the webinar was very instructive and you can watch it here.

The BIG difference for us patients is that no matter what, out-of-pocket drug costs for 2025 cannot exceed $2000. You heard right – for those of you on specialty oral medications like Nubeqa (darolutamide for prostate cancer) or Aubagio (teriflunomide for MS), normally sourced via specialty pharmacies, you will meet this cap January. And you’ll even be able to spread the payment over 12 months! More on that to follow.

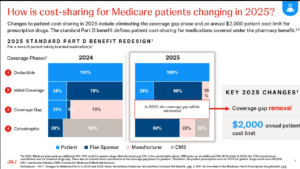

But first, how is this coming about. Well it tracks back tot he changes brought about by the Inflation Reduction Act signed by President Biden in 2022. He promised to make drugs more affordable, and this is a part of the plan. As you can see in the slide to the left comparing 2024 to 2025, the donut hole has been eliminated. In its place, the Payer (Plan Sponsor) and Pharma (manufacturer) are paying more. While the cost saving is very positive, it will likely impact us patients in other ways:

Your formulary choice may be reduced – so CHECK your medications before you renew.

Premiums for Part D may increase – even though out of pocket is capped. If you are unlikely to spend $2,000, look for a plan that defers your co-pay as long as possible

Higher premium plans should cover a larger portion of drug costs earlier. Your premium does NOT count towards the $2,000, so include premiums in your cost calculation to figure your exposure.

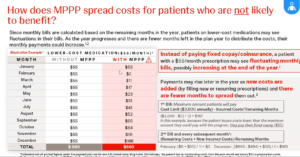

If you have a co-pay or co-insurance on your drugs, no matter if it’s Part C or D, it cannot exceed $2,000. However the amount you pay and who you pay it to may become a bit of a moving target. We mentioned earlier that you will now have the opportunity to spread your payments over the calendar year – or the remainder of it, if you sign up late or incur costs late in the year. The Medicare Prescription Payment Plan (M3P) takes your share of drug costs, up to a maximum of $2,000, and spreads them over the remainder of the year.

The simple example is for those on specialty pharmaceutical drugs like Nubeqa or Aubagio. Since your share of the drug cost is almost certainly going to be greater than $2,000 in January, if you opt in for M3P BEFORE going to the pharmacy or ordering from your mail order pharmacy, you’ll pay nothing on picking up/shipping the drugs. Subsequently, you’ll get a separate bill from your Payer for $167.67 monthly over 12 months, and pay no more for any of your drugs the rest of the year. There is NO interest, no late fee penalties, and you get a couple of months leeway, but there are penalties if you never pay. You can sign up for MP3 with your Medicare Payer/Plan Holder BUT not in the pharmacy for 2025. So if you arrive at the drug store prior to enrollment, you’ll be charged $2,000 to take your pills home. You can leave the pills, go home, enroll and return to the pharmacy 24 hours later and pick up without payment to the pharmacy..

If you don’t start this expensive drug until mid year, say September, and you’ve spent nothing on drugs prior, then the $2,000 is billed over the last 4 months at $500/month.

But what if your drug costs are more lumpy – they go up and down the whole year. In that case, the payments get recalculated each month and the monthly bill will vary.

There is a strange case too, if you know your co-pay is the same each month – say $55. This really throws M3P, and as you can see to the left, you’ll pay the same $660 (12x $55) either way but in different amounts each month if enrolled in M3P.

Finally, let’s address the Drug Benefit plans that many of you enjoy through PAN, PAF and others. Even the drug discount cards from Pharma that some receive. Whatever you receive, or however you receive it, does NOT reduce your $2,000 exposure. You advise the pharmacy that you have a benefit, and they bill the Benefit Provider (PAN, PAF, Pharma ??). The credit will be applied against your drug cost, although eventually you may still be liable for up to $2,000 co-pay when the benefit runs out.

Looking at the first slide, it seems to AnCan that these benefits that are often funded by Pharma, eventually flow back to Pharma and the Payer. How they will credit them against what the patient owes is not yet clear. Before you get too crazed, our guess is the system has to change. These benefits need to be channeled directly to patients who cannot afford $2,000 p.a. AnCan is on it and already reaching out to NAMAPA and others to promote more of a direct, income based subsidy possibly reaching more beneficiaries. One thing we have heard – APPLY EARLY for 2025 in the event you are in line to receive a subsidy.

PLEASE BE SURE TO SIGN UP FOR THE M3P PROGRAM UPFRONT. EVEN IF YOU OWE $2,000 IT WILL BE BILLED IN 12 INSTALLMENTS. WE STILLL HAVE TO FIGURE HOW YOU WILL BE REIMBURSED IF YOU RECEIVE ASSISTANCE.

IF YOU HAVE A GRANT BE SURE TO PROVIDE DETALS TO THE PHARMACY ASAP. NOTWITHSTANDING, ALSO REACH OUT TO YOUR GRANTOR TO FIND HOW THEY WANT TO COORDINATE THE GRANT. IT’S STILLL A MOVING TARGET!

With Open Enrollment starting on October 15, two AnCan’rs asked for advice this week on Medicare plans – and yes it’s complicated. AnCan recommends you watch the webinar we held last October to help understand the difference between traditional Medicare and Medicare Advantage. The dollar details are different for 2025 but not the principles.

Lastly, my own health insurance broker, Kim Umphres, is licensed to write in 15 States. He offered his help to all in last year’s webinar, so take him up umphres100@yahoo.com

Since the same questions are likely in the mind of many others, I have written this Blog Post. I am no expert but this may illustrate how I think about my own health insurance. Sadly, I cannot help you all individually – consult with your own Medicare health insurance for the best advice.

Onward & upwards, rick

Many of us on Medicare are faced with renewing our plans – or buying a plan for the first time. If you choose not to buy a plan to supplement Medicare, it leaves you exposed to roughly 20% of your medical costs. That can amount to very big bucks!

The main choice is whether to opt for Traditional Medicare + a Supplement (Medigap) Plan + a Drug Plan. Alternatively, a Medicare Advantage Plan can look attractive but comes with warts.

If you are low income and cannot afford the available plans, there are Medicaid alternatives for Medicare supplements.

Advantage Plans (Plan C) restrict your choice of Health Care Providers since they are based on Provider Networks. If you need a particular type of specialist, for example a genitourinary medical oncologist, or a neurologist who specializes in MS, this can be a problem with Advantage. Community Standard of Care is often the byword. If you choose an Advantage Plan, be sure it covers HCPs who practice at a Center of Excellence.

Advantage Plans usually have small monthly premiums, sometimes zero. They also include co-pays when you visit a Provider. Co-pays can be anywhere from Zero dollars to several hundred for fancy scans like PSMA, so you have to look carefully at the coverage. The more you use the plan, the more you pay. Some may include coinsurance – avoid those altogether. It’s a nuance we won’t get into here.

You can also go out of network to a Provider of your choice, but copays will be significantly higher. For example, you may pay $50 for a visit to a specialist in-network. Out-of-network, the cost can be significantly higher – often 40% of the approved Medicare fee for the service sought.

Advantage Plans often have a Gatekeeper who must approve any referral. You may not be able to self refer. Also there can be stricter intervention by the Plan to pre-approve procedures.

Drugs are included, however there is also a co-pay for some generic and all branded drugs that depends on the tier in which they are classified in the Plan’s drug formulary. List the drugs you use and find the cost. That said, the good news in 2025 is that drug out-of-pocket costs cannot exceed $2,000.

Traditional Medicare with a Supplement (Plans F,G,K,L,M,N) may not restrict your choice of HCPs – you can go anywhere in or out of state provided the Provider accepts Medicare.

Traditional Medicare Supplement Plans cover the 20% not covered by Medicare A and B. You pay a monthly premium that varies according to the plan chosen. The different supplement plans have different features. The more you pay in monthly premium, the less the restrictions and the lower the deductibles.

In addition you will need drug coverage (Plan D). Again that includes a monthly premium, plus a charge for each drug, so you have to shop plans against your Rx. For 2025, drug out-of-pocket costs cannot exceed $2,000.

As long as your chosen Provider accepts self-referrals, there may be no Gatekeeper. Procedures and protocols may still be subject to pre-approval.

Since Advantage Plans can be more profitable for the Payer, they offer lots of bells and whistles to sell the plan – for example subsidies for OTC products. One plan I was offered recently, actually pays the Holder $5/month!

I’m trained as an economist so I look at risk reward. I compare the annual maximum out-of-pocket cost between the Advantage Plan and the Traditional Medicare Plans (inc. the drug plan).

For traditional Medicare There is a required monthly premium for both the Supplement and the Drug Plan. Add those together and multiply by 12. In addition you can have out-of-pocket drug costs, especially if you are using expensive cancer drugs, but that cannot exceed $2,000 in 2025. Btw, the $2000 will decrease in subsequent years.

Each Advantage Plan has a stipulated maximum out-of-pocket cost for in-network and out-of-network Providers. In-network will be less. I look at the out-of-network max, and add to that any monthly premiums that are usually minimal. Drugs are included with a co-pay, but that co-pay cannot exceed $2,000 in 2025.

Now that I know what I HAVE to pay with Traditional + Supplement vs what I could pay with Advantage depending on my usage, I can compare whether I want to roll the dice to save money.

If the Traditional route costs me $500 in monthly premiums, I know I am out-of-pocket $6,000 plus my drug copay costs capped at $2,000.

Say my Advantage Plan has a monthly premium of $25, then for sure I am out of pocket $300. The rest depends on how much medical care I use. Assume ( the economist’s favorite word) the out-of-pocket for out-of-network in my plan is $8,000, that is my max. I still have to consider up to $2,000 for drugs.

Let’s compare!

IN THE WORST CASE I am spending $6,000 (+ drugs) for Traditional Supplement versus $8,300 (+ drugs) for Advantage. The Advantage could be $2,300 more pricey.

IN THE BEST CASE, I am out-of-pocket $300 (+ drugs) for Advantage vs $6,000 (+ drugs) for Traditional Supplement, so I could save $5,700 with Advantage.

Risk-Reward… do I want to roll the dice to save up to $5,700 that could cost me an extra $2,300??

Each person has to make that decision.

There’s more to it than this. For example HMO’s like Kaiser Permanente may make it even harder to go out of network. And with KP, you are guarantied to only get community Standard of Care medicine . As I often say, KP is great as long as you don’t get seriously ill.

AnCan strongly suggests finding a local Medicare Health Insurance Agent to help you sort through this morass. Plans change by State, so your agent must be licensed in your State.

And one last thing. The first time you enter Medicare there is NO underwriting. No matter your preconditions, you are accepted to any Traditional supplement or Advantage Plan. In subsequent years, you may be subject to underwriting should you choose to switch plans. You can be restricted from changing between an Advantage and Traditional Supplement Plan.

AnCan recommends watching our webinar from last October to help understand the difference between traditional Medicare and Medicare Advantage. 2025 details are different but not the principles.

We also recommend you visit the Triage website and attend its free webinars. Many of their Medicare resources can be found at https://triagecancer.org/medicare-cancer

For differences between the Traditional Supplement Plans, consult with a specialized Medicare Health Insurance agent. F and G are the best options. There are also high deductible options. An agent can also help you compare Advantage plans by various criteria, like maximum out-of-pocket for out-of-network care.

Off-Label Use vs. Unapproved Use

Off-Label Use vs. Unapproved Use

AnCan Foundation, the innovator of virtual support groups, is coming to our 10th Anniversary in less than 10 months. We’ve grown – about one-third of US nonprofits fail in that time, and we have flourished. Starting with 3, or was it 4, meetings, AnCan now boasts 33 virtual monthly events for 16 different conditions. If that’s not evidence enough, annually we serve around 7,000 live; approx. 33,000 through our recordings, and we have close to a half-million who make contact with the AnCan logo somehow or other annually. That’s a lot. Watch out for our new Impact Report that’s in the works.

AnCan Foundation, the innovator of virtual support groups, is coming to our 10th Anniversary in less than 10 months. We’ve grown – about one-third of US nonprofits fail in that time, and we have flourished. Starting with 3, or was it 4, meetings, AnCan now boasts 33 virtual monthly events for 16 different conditions. If that’s not evidence enough, annually we serve around 7,000 live; approx. 33,000 through our recordings, and we have close to a half-million who make contact with the AnCan logo somehow or other annually. That’s a lot. Watch out for our new Impact Report that’s in the works.

and this is a part of the plan. As you can see in the slide to the left comparing 2024 to 2025, the donut hole has been eliminated. In its place, the Payer (Plan Sponsor) and Pharma (manufacturer) are paying more. While the cost saving is very positive, it will likely impact us patients in other ways:

and this is a part of the plan. As you can see in the slide to the left comparing 2024 to 2025, the donut hole has been eliminated. In its place, the Payer (Plan Sponsor) and Pharma (manufacturer) are paying more. While the cost saving is very positive, it will likely impact us patients in other ways: But what if your drug costs are more lumpy – they go up and down the whole year. In that case, the payments get recalculated each month and the monthly bill will vary.

But what if your drug costs are more lumpy – they go up and down the whole year. In that case, the payments get recalculated each month and the monthly bill will vary.